Banks are a major part of the Australian economy owing to their pivotal role in providing loan and deposit products to savers and borrowers across the country. They are also a large component of the Australian share market given their role as a major source of dividends for share investors, and the fact that they comprise approximately 20% of the Australian share market by value.

Three of Australia’s four major banks – ANZ, NAB and Westpac – recently reported their half year results for the period to 31 March 2022. This gave us a good insight into how the banks are performing, and it helped us form a view on the future level of returns that we can expect from them. Note that Commonwealth Bank has a different reporting period, and hence it will report its next set of profit results in August 2022.

Overall, we thought the results were good. In this article, we discuss some of the key features of the results, along with the market’s reaction to the reported results and our current investment view on the bank sector.

Key features of bank results

Australia’s banks make most of their profit from ‘Net Interest Income’. This is basically the spread that banks earn between the rate at which they lend money to borrowers (for example, from housing and business loans), over the rate at which they borrow money from savers (for example, from customer deposits in savings accounts and term deposits). This is arguably the most important line in the profit and loss statement for an Australian bank.

NAB had the highest growth in Net Interest Income for the period at 4%. This was the result of strong growth in its total amount of loans made to customers. Westpac’s Net Interest Income was the worst of the reported results, as it had to cut its lending rates to grow its loan book.

See Graph: Major Banks, Net Interest Income Growth

These ‘Net Interest Income’ results effectively drove the bottom line ‘Net Profit After Tax’ results. Both ANZ and NAB delivered 4% profit growth, while Westpac’s reported profit fell by 12%.

See Graph: Major Banks NPAT Growth

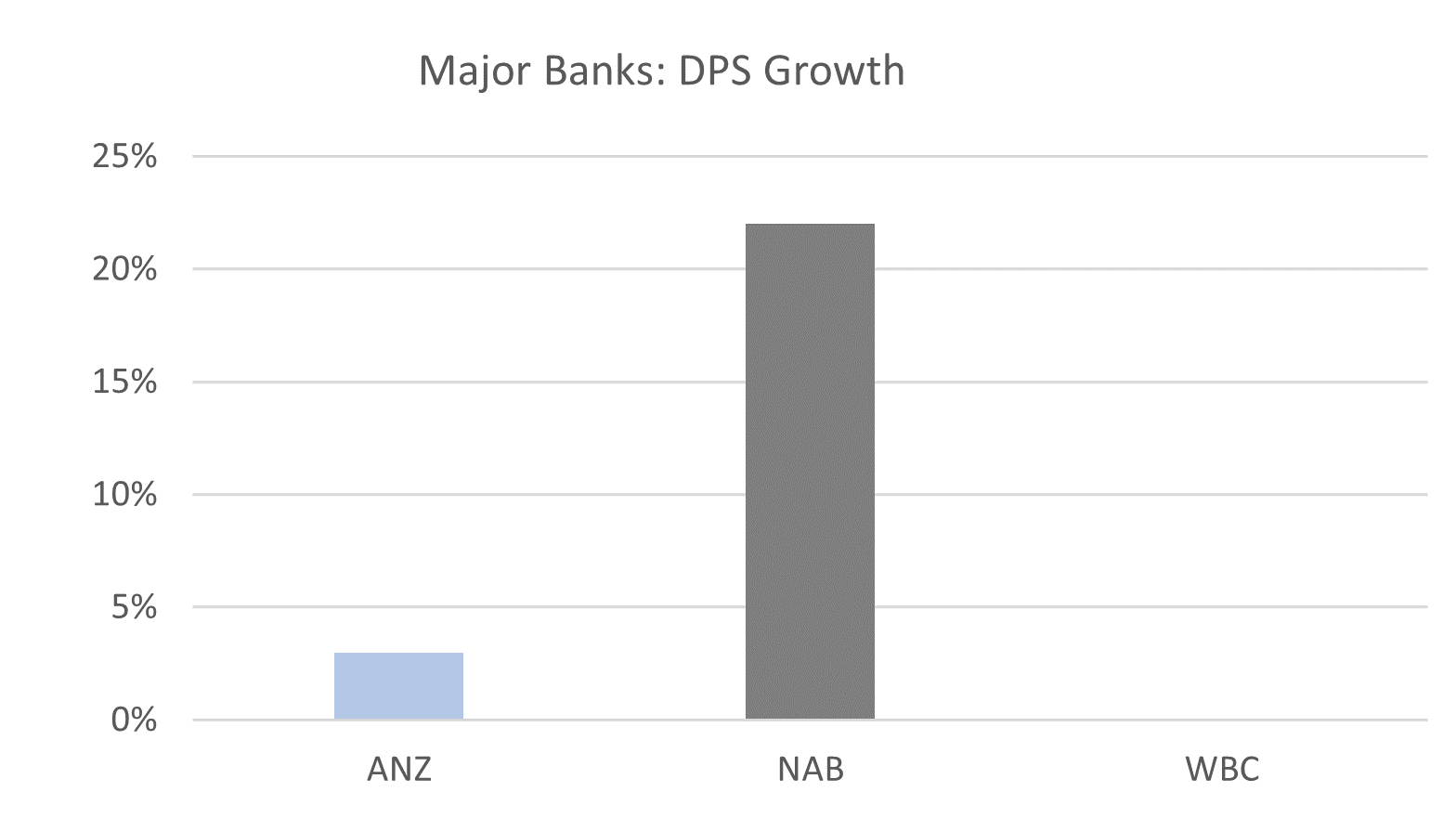

Bank dividends are a major source of income for many share market investors, and these bank dividends are largely an outcome of bank profits. NAB’s dividend grew the most this period at 20%, a function of the profit growth discussed above alongside an increase in the dividend payout ratio.

ANZ’s dividend growth was more ‘normal’ at 3%, largely in line with its profit growth. Westpac’s dividend was flat compared to last year’s period.

See Graph: Major Banks DPS Growth

In terms of returns, NAB is currently producing the highest ‘Return on Equity’ at 11.3%, followed by ANZ at 10.0% and Westpac at 8.7%.

See Graph: Major Banks Cash ROE

Costs were a major focus as always for the market during the results period. In this area, there was a clear divergence in results and management commentary. Westpac reiterated its cost reduction target, whereas ANZ and NAB moved away from their previously announced cost targets.

In terms of Cost to Income ratios, NAB is running the most efficiently at 45%, with ANZ and Westpac well behind at 54%.

See Graph: Major Banks Cost To Income Ratio

Bad debts are usually a focus of bank results, but they were largely non-existent in this set of results. The Australian economy is currently in very strong shape, as evidenced by the very low unemployment rate. This has been of large benefit to the banks.

We focus on the ‘Collective Provisions as a % of Credit Risk Weighted Assets’ metric to assess whether the banks are adequately provisioned. NAB has the best provision coverage followed by Westpac and ANZ, with all three in a good position.

See Graph: Major Banks Collective Provisions as % CRWA

The banks’ balance sheets are all in good shape. Common Equity Tier 1 Ratios are above 11.0%, which is higher than required by the prudential regulator APRA.

See Graph: Major Banks CET1 Ratio

Market reaction

Westpac had the best share price performance during the results period. While the key metrics reported by Westpac looked poor on the surface, they were better than what the market was expecting. Additionally, they indicated that Westpac are progressing on a path towards delivering better returns over the medium term.

Our investment view

At the sector level, we think the banks are in good shape in terms of their simplified businesses and solid balance sheets. As such they look capable of delivering good income returns to investors over the medium term. But we think that growth becomes more challenged over the long term, reflecting the sector’s maturity and the persistently high competition to the banks’ traditional revenue streams.

At the stock level, we think ANZ, NAB and CBA are fairly valued. Westpac stands out to us as representing the most attractive value. If it can deliver most of its strategic objectives, including a significant reduction on costs, then we think it can deliver strong growth in dividends and a better return on equity.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}